US Dollar Index looks bid near 109.00 ahead of key data

- The index regains the smile and flirts with the 109.00 region.

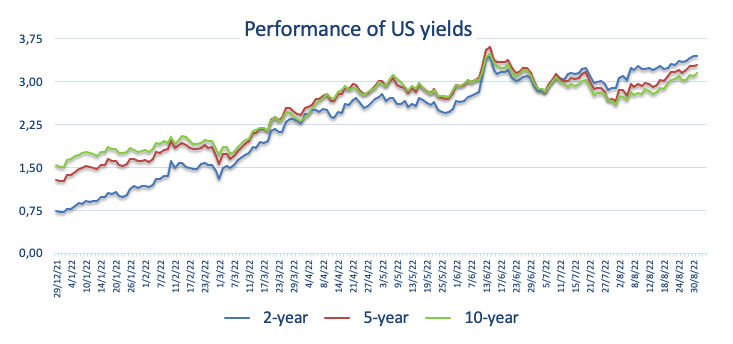

- US yields look to extend the ongoing uptrend on Thursday.

- ISM Manufacturing will be the salient event later in the docket.

The greenback extends the choppy performance so far this week and now lifts the US Dollar Index (DXY) back to the 109.00 neighbourhood on Thursday.

US Dollar Index looks to ISM results

The index leaves behind Wednesday’s pullback and resumes the upside in the 109.00 region helped by the knee-jerk in the risk-associated galaxy and the continuation of the march north in US yields across the curve.

In fact, the index manages well to keep the trade within a side-lined theme in the upper end of the recent range, always underpinned by rising expectation around the Fed’s tightening plans, while recession chatter usually limiting the upside potential.

Data wise in the US, usual weekly Claims are due in the first turn ahead of the always-relevant ISM Manufacturing for the month of August, the final S&P Global Manufacturing PMI and Construction Spending.

In addition, Atlanta Fed R.Bostic (2024 voter, centrist) is also due to speak.

What to look for around USD

The greenback remains within a consolidative phase around the 109.00 zone so far this week after retreating from Monday’s fresh cycle peaks around 109.50 when tracked by the US Dollar Index (DXY).

Bolstering the dollar’s strength appears the firm conviction of the Federal Reserve to keep hiking rates until inflation looks well under control regardless of a likely slowdown in the economic activity and some loss of momentum in the labour market. This view was recently reinforced by Chair Powell’s speech at the Jackson Hole Symposium.

Extra volatility in the dollar, however, should not be ruled out considering the ongoing debate around the size of the September’s interest rate hike by the Federal Reserve.

Looking at the more macro scenario, the greenback appears propped up by the Fed’s divergence vs. most of its G10 peers (especially the ECB) in combination with bouts of geopolitical effervescence and occasional re-emergence of risk aversion.

Key events in the US this week: Initial Claims, Final Manufacturing PMI, ISM Manufacturing, Construction Spending (Thursday) – Nonfarm Payrolls, Unemployment Rate, Factory Orders (Friday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation over a recession in the next months. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

US Dollar Index relevant levels

Now, the index is advancing 0.22% at 108.92 and a break above 109.47 (2022 high July 15) would aim for 109.77 (monthly high September 2002) and then 110.00 (round level). On the other hand, the next contention turns up at 107.58 (weekly low August 26) seconded by 106.59 (55-day SMA) and then 104.63 (monthly low August 10).